Congress asked the Government Accountability Office (GAO) to assess the cost of the 2007 financial crisis and if the 2010 Dodd-Frank legislation will prevent future crises. GAO just released their findings: “the present value of cumulative output losses could exceed $13 trillion” and “[there is] no clear consensus on the extent to which, if at all, the Dodd-Frank Act will help reduce the probability or severity of a future crisis”. $13 trillion? If at all? That’s alarming.

GAO studied not just the bailout cost, which looks to be $1.5T to $3T, but the overall cost. “While the structural imbalance between spending and revenue paths in the federal budget predated the financial crisis … From the end of 2007 to the end of 2010, federal debt held by the public increased from roughly 36 percent of GDP to roughly 62 percent. Key factors … included (1) reduced tax revenues … (2) increased spending on unemployment insurance … (3) fiscal stimulus programs … (4) increased government assistance to stabilize financial institutions and markets.” 36% to 62% is one big jump.

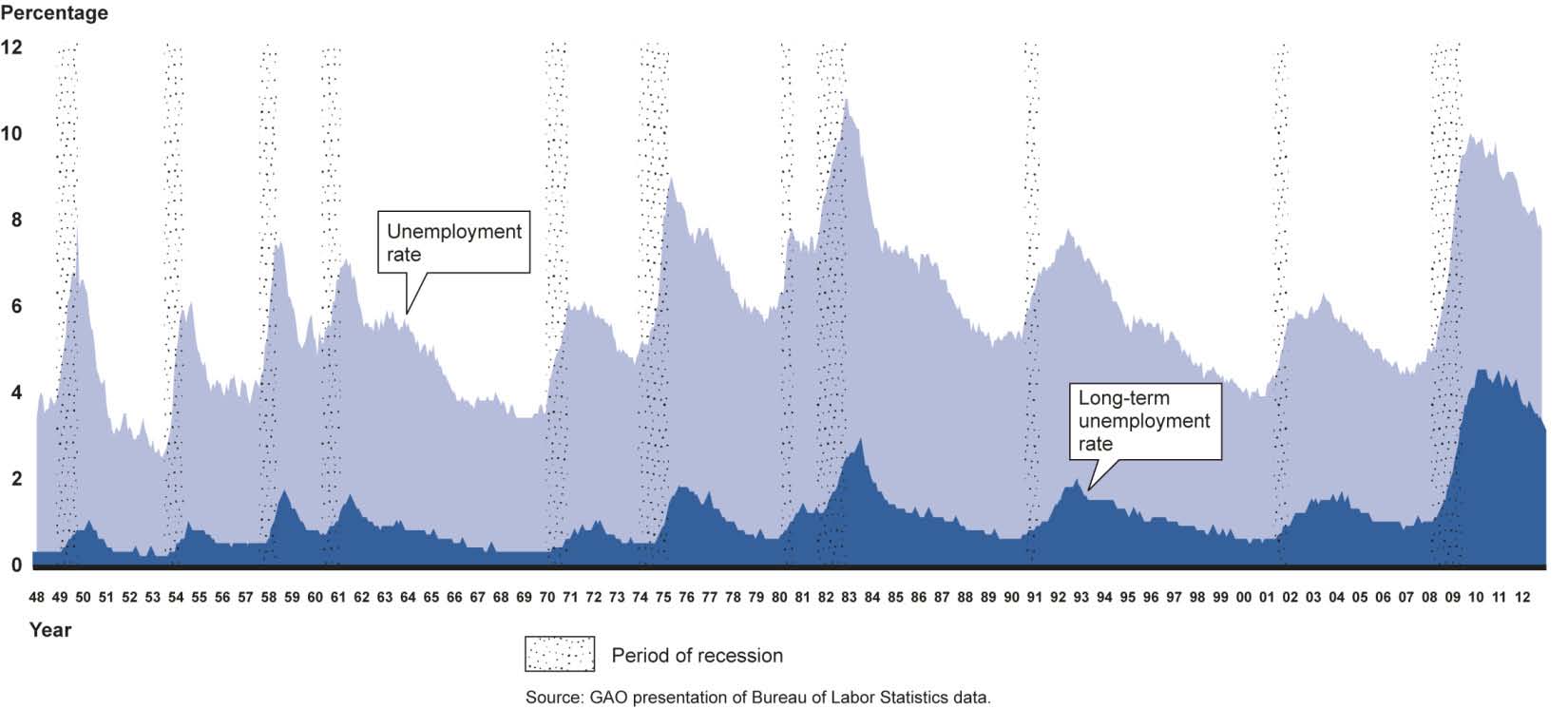

Consumer spending (70% of our economy) fell, GAO notes, because: “median household net worth fell by $49,100 per family, or by nearly 39 percent, between 2007 and 2010”. They also show the high human cost of long-term unemployment from the financial sector’s collapse.

Maybe later I’ll explore why Congress passed legislation GAO found may or may not “reduce the probability or severity of a future crisis“, legislation that is both enormously too complex and not what we normally think of as regulation. The Glass-Steagall Act that transformed finance after the 1929 Wall Street Crash has 37 pages. Dodd-Frank has 848 and does not specify rules people must follow but new regulations bureaucrats must create along with enforcement agencies. That’s not how we do things where I’d like to come from.

Maybe later I’ll explore why Congress passed legislation GAO found may or may not “reduce the probability or severity of a future crisis“, legislation that is both enormously too complex and not what we normally think of as regulation. The Glass-Steagall Act that transformed finance after the 1929 Wall Street Crash has 37 pages. Dodd-Frank has 848 and does not specify rules people must follow but new regulations bureaucrats must create along with enforcement agencies. That’s not how we do things where I’d like to come from.

The immediate, urgent question is, what must we make Congress do instead? Now I understand the problem (see previous pasts), the solution looks pretty straightforward:

- Eliminate too-big-to-fail. The collapse of the big banks and AIG threatened to paralyze our entire economy. They were bailed out because they were considered too big to be allowed to fail. Businesses that go wrong should fail. And they should fail without damaging the economy. This means banks must be limited to a maximum of, say, 5% of total US deposits and any that become insolvent must be forced into receivership under the FDIC.

- Regulate derivatives. The collapse of any one financial institution could trigger the collapse of the whole system because inter-dependencies via derivatives were gigantic and invisible to regulators. To make them visible, derivatives must be traded on exchanges like stocks and futures, and ones that could require a future payout must be treated like insurance with their underwriters required to carry reserves.

- Restore 12:1 leverage. The big banks failed so fast because their capital reserves were too low. Our economy depends on lending and they had to stop when they became insolvent. The SEC waiver of the 1975 net capitalization rule must be reversed and SEC discretion over the rule must be eliminated.

- Restore Glass-Steagall. Tax-payers have to foot the cost of the mega-banks’ mismanagement because speculation and underwriting is no longer separate from taxpayer-backed depository banks. The separation must be restored.

- Regulate non-bank lenders. Many of the loans most likely to default were originated by non-banks who securitized and sold them. Any institution that originates a loan must be required to keep, say, 10% of its securitized loans and absorb the first 10% of default losses incurred by investors in the securitized loans.

Among other things, the Dodd-Frank Act mandates the SEC to require US public companies to repossess executives’ short-term profits that result in long-term liabilities that require an accounting restatement. There is also discussion of ways to make senior management personally liable in the event of a taxpayer bailout. I have little confidence in either approach. Compensation committees will indemnify executives from such provisions. Shareholders and taxpayers will continue to pay.

The Justice Department recently sued S&P for up to $5B for defrauding investors with inflated credit ratings. I assume Moody’s will also be sued because they, too,were paid for ratings by investment banks that issued mortgage securities. We might hope S&P and Moody’s will change the way they do business to eliminate the conflict of interest. More proactive would be to open the ratings business to competition.

Hmm, my Buddhist practice must be helping – I got through exploring all this Washington/Wall Street malarkey without feeling angry. I feel wrathful determination to do whatever I can to get it fixed, but wrath can be positive.

Fixing the negatives will discourage allocation of capital where it will have little or no value. Next I’ll turn to the positive and explore what could guide good allocation.

Our too-big-to-fail banks are twice as big even as they appear. If they had to conform not to US-specific but to international accounting rules for off-balance-sheet assets and derivatives, the bets that blew up and triggered the 2007 financial crisis, JPMorgan, Bank of America, and Wells Fargo would double in assets, and Citigroup Inc. would jump 60%. Their combined assets would be $14.7T, which is 93% of US GDP.

Source: http://www.bloomberg.com/news/2013-02-20/u-s-banks-bigger-than-gdp-as-accounting-rift-masks-risk.html

We are very, very foolish to continue allowing too-big-to-fail banks to exist.

This is encouraging, Senators Brown and Vitter from opposite ends of the political spectrum, are working on bipartisan legislation to fix the too-big-to-fail banks problem:

http://www.huffingtonpost.com/2013/02/28/sherrod-brown-banks-david-vitter_n_2782665.html?utm_hp_ref=politics

I agree with your emphasis on too-big-to-fail and your five points of solution, but it’s not fair to blame the 2007 financial crisis for all of the increase in federal debt. After all, you went to great lengths to show the contributions made by wars-of choice and entitlements such as Medicare cripppled by rising health care costs. Let’s not forget that tax cuts were a significant cause of “reduced tax revenues” as well.

I haven’t yet figured out how best to establish hierarchy with this platform. I’d put “Financial System” on the same level as the topics you cite, wars-of-choice, tax cuts and healthcare. It’s one of the areas where we must make big changes.

Maybe I should add an Executive Summaries category with posts of conclusions that link to posts that support them? That feels clumsy but maybe is worth a try.

The majority of posts will always be on relatively narrow aspects of a larger topic. I’ve started trying to post them as series, which does seem useful. But posts disappear from view behind newer ones.

I guess this is why books were invented, but now we’re in a world of e-books and that’s a topic for exploration in its own right.

I’d be very grateful for any suggestions about blog architecture.

Martin, I’m just getting around to reading this series of papers you’ve written on the characteristics of our economy and the causes for the morass into which it has fallen. I’m impressed with your meticulous research and your condensation of a complex subject into what constitutes a useful primer on the subject. I agree with your five points for fixing the problems, but I would add a sixth having to do with the ratings given MBSs (Mortgage-Backed Securities) and CDOs (Collateralized Debt Obligations) and other securities of that ilk.

You briefly mentioned the S&P suit. The Financial Crisis Inquiry Commission reported in January 2011 that:

“The three credit rating agencies were key enablers of the financial meltdown. The mortgage-related securities at the heart of the crisis could not have been marketed and sold without their seal of approval. Investors relied on them, often blindly. In some cases, they were obligated to use them, or regulatory capital standards were hinged on them. This crisis could not have happened without the rating agencies. Their ratings helped the market soar and their downgrades through 2007 and 2008 wreaked havoc across markets and firms.”

As you mentioned earlier, two ways that ratings agencies were able to give high ratings to “junk” securities were that they ignored the possibility of a housing bubble/meltdown and they assumed that “insurance” in the form of CDSs (Credit Default Swaps) and other such instruments would overcome the negative aspects of underlying mortgage loans to homeowners with bad credit and undocumented incomes.

A useful addition to your five points would be to require that such securities have an overall rating based solely on the quality of the underlying loans and that the prospectus list the percentage of underlying loans in each of n ascending quality categories (e.g. F-rated to AAA-rated). Commentary could be added to the prospectus discussing the effect “insurance” and the expected condition of the housing market over the lifetime of the security would have on its credit-worthiness.

In March 8 hearings about the Administration’s response to socially undesirable activities by the TBTF banks, Senator Warren began:

“Now in December, HSBC admitted to money laundering. To laundering $881 million that we know of for Mexican and Colombian drug cartels. And also admitted to violating our sanctions for Iran, Libya, Cuba, Burma, the Sudan. And they didn’t do it just one time. It wasn’t like a mistake. They did it over and over and over again across a period of years. And they were caught doing it. Warned not to do it. And kept right on doing it. And evidently making profits doing it. Now HSBC paid a fine, but no one individual went to trial. No individual was banned from banking. And there was no hearing to consider shutting down HSBC’s activities here in the United States.”

How much crime would be too much, she repeatedly asked the Treasury Undersecretary for Terrorism and Financial Crimes? He said Dept of Justice must decide such things and would give no opinion.

Senator Warren concluded: “I’ll just say here, if you’re caught with an ounce of cocaine, the chances are good you’re going to go to jail. If it happens repeatedly you may go to jail for the rest of your life. But evidently, if you launder nearly a billion dollars for drug cartels and violate our international sanctions, your company pays a fine and you go home and sleep in your own bed at night. Every single individual associated with this. I just, I think that’s fundamentally wrong.”

Video: here

Text: http://www.ritholtz.com/blog/2013/03/90213

Here’s an excellent piece about the “Terminating Bailouts for Taxpayer Fairness (TBTF) Act of 2013” introduced by Senators Sherrod Brown, an Ohio Democrat, and David Vitter, a Louisiana Republican.

http://www.washingtonpost.com/business/can-two-senators-end-too-big-to-fail/2013/05/09/aa01cc70-b5dc-11e2-b94c-b684dda07add_story.html

What’s great about this Act is its simplicity and that it’s supported by a diverse set of interests, including a large part of the banking community itself. It could actually pass, and if it does become law, it could be enforced!

The Act’s key provisions are:

●Mandates a flat 15 percent capital requirement for any institution with more than $500 billion in assets

●Does not rely on ratings agency grades

●Removes off-balance-sheet assets and liabilities as different classes — they are treated as if they are on the balance sheet

●Requires derivatives positions to be included in a bank’s consolidated assets

●Requires that the capital cushion a bank holds be liquid