Do we really need Social Security? Is it fair that it is mandatory or that high earners contribute more but get relatively less benefit? What is the best way to keep it financially sound? What guidance does it offer to make our overall tax and budget management system better?

Do we need Social Security? It is different from other government programs in that its costs are matched by dedicated taxes. Hoping to stimulate consumer spending, we recently cut them temporarily. Should we eliminate them altogether? It would be time-consuming and costly, but we could in theory unwind the program and for example, switch to a system like Nepal’s where families traditionally support each other.

That thought experiment highlights the parallel between contemporary Nepal and pre-industrial USA. Both are family farm economies where when you retire, your kids take over and support you. In a society where generation after generation works on the same farm, if you are unable to work when your kids are young, a relative can take over and neighbors help when family is not enough. In an economy of jobs, however, workers create no family asset to take over, people keep moving, families become dispersed and communities exist mainly in virtual space.

Nepal’s situation is thought-provoking, too, because its traditional support system is collapsing. The 1996-2006 civil war made villages too dangerous so people abandoned their farms and moved to the cities. They now need jobs but Nepal has no industry because there is insufficient power (no electricity 14 hours a day), insufficient access to market (no railroad and extremely weak roads), a corrupt legal system and no government. So Nepalis go overseas for jobs and send money to their families. That is currently a quarter of the entire economy. But they send less as they form new attachments.

In the USA we have a job-producing infrastructure but we are vulnerable to losing our job, our family is probably far away, and few of us save enough for retirement. Like other Western societies, the nature of our economy makes us dependent on social security when we cannot support ourselves.

Is it fair that Social Security is mandatory? It seems so in a society like ours. We simply don’t save enough voluntarily – 7% or more of every $ we ever earn, invested to earn at least 3% above inflation, as noted here: Our Ridiculous Approach to Retirement. And we don’t have enough disability insurance. The result? “Almost half of middle-class workers, 49 percent, will be poor or near poor in retirement, living on a food budget of about $5 a day”. That’s even with social security benefits.

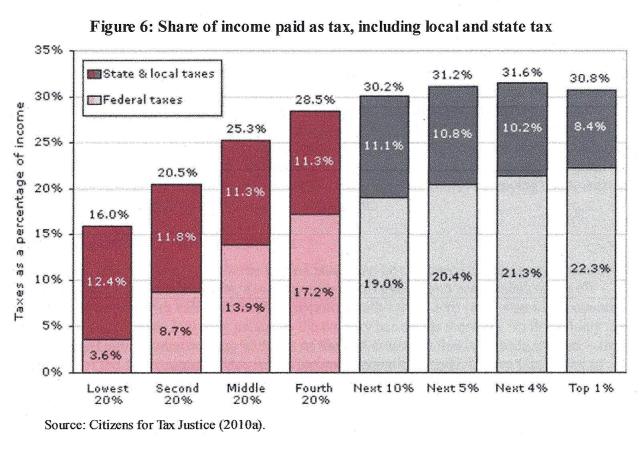

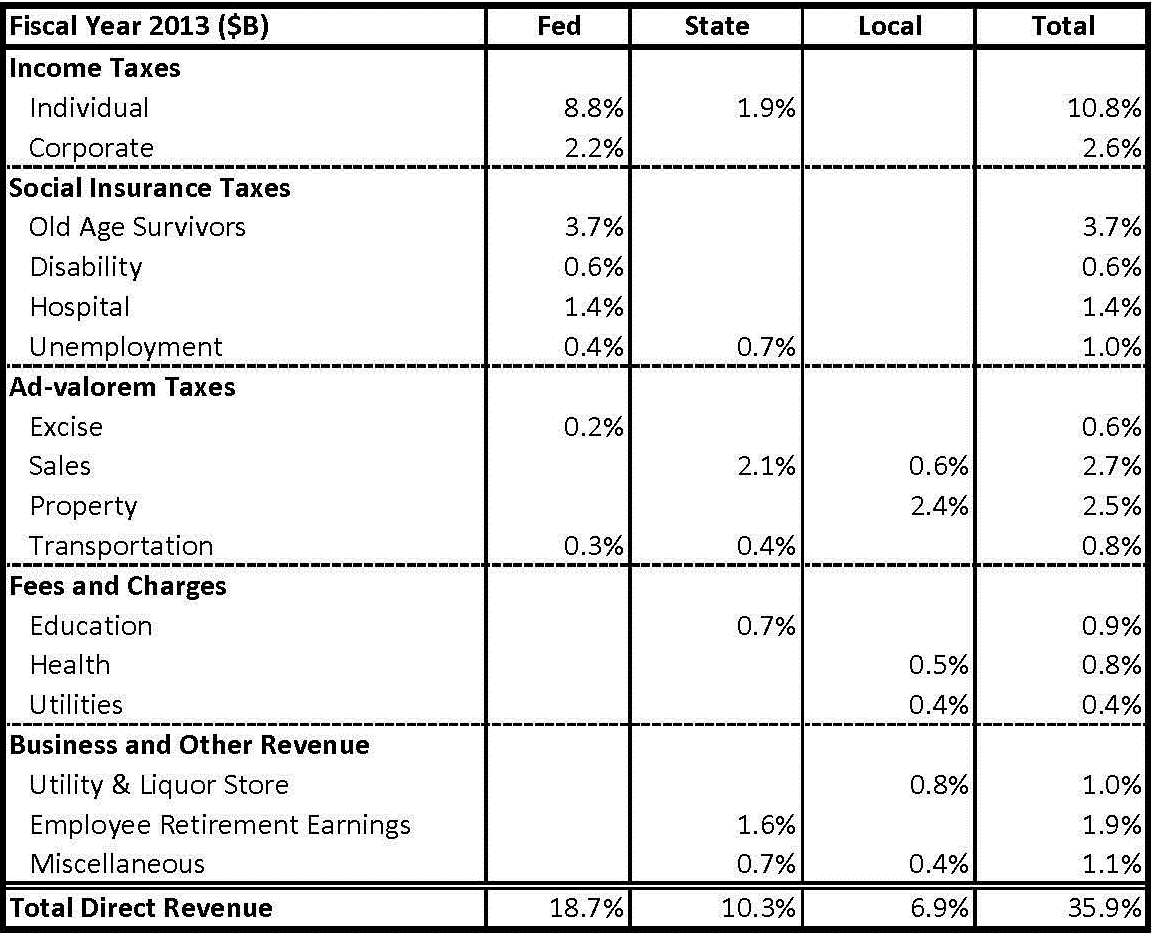

Is it fair that high earners contribute more but get the same benefit as those who contribute less? We all contribute at the same % rate but the higher our income, the more we contribute in total. The more we contribute, the higher our monthly benefit, but those who contribute more get proportionately less. We get 90% of the first $X (currently $791) of our average monthly earnings, 32% of the next $Y of earnings (currently the the amount between $791 and $4,768), and 15% of the remaining $X (currently the amount over $4,768) – see Social Security Benefit Amounts. Is that fair?

That question may be the most contentious. Should those with higher earnings pay taxes at the same or a higher rate? I will return to this when I explore income tax. Here, I’ll just make an observation in this context. Everyone’s work adds assets to our economy. If it is reasonable to consider those with higher earnings to be getting a higher return on those assets, it is reasonable they should contribute more to the ongoing development of the assets. I can’t be the first to have this thought. I’d be grateful for a discussion of its merits, if any.

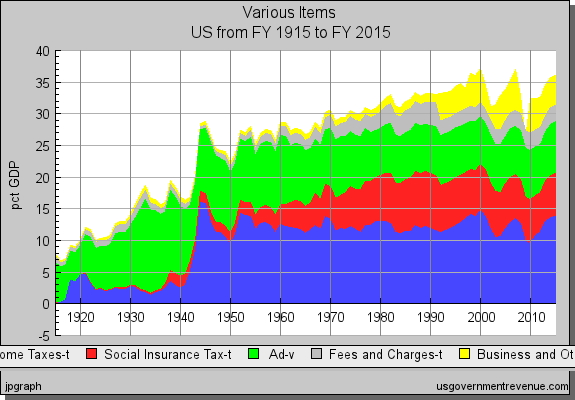

What is the best way to keep Social Security financially sound? Social Security will take in roughly $40B more than it pays out in 2013, so it is not contributing to the problem I noted in FY2010 Revenues, Expenses and Liabilities: “Federal revenue last year was $2.2T while expenses were $3.5T. We therefore increased public debt by $1.3T.” Although the Social Security’s trust fund is growing now and will be around $2.8T in 2013, that will not always be the case. As I noted in Social Security: “Social Security taxes [were sufficient] to pay current recipients … until 1975 – 1981 when expenses exceeded revenue every year. Average benefits were then cut approx 5%, tax rates for individuals were raised approx 2.3%, and the full retirement age was raised 3%, which created an annual surplus until 2009.” Another update will be necessary.

“The fundamental problem”, I wrote, “is that while 100 workers supported only 6 Social Security beneficiaries in 1950, 100 workers in 2010 must support 33 beneficiaries. When the Social Security full retirement age was set at 65 in 1935, USA life expectancy at birth was 62. The retirement age is now 67 but life expectancy is 78. “ In Social Security – Past and Future Changes I explored our options.

The best way is to increase the payroll tax ceiling and raise the tax rate. I won’t repeat the analysis here, just add that Social Security finances are far more predictable than other government programs. We can model population trends, which change relatively slowly, and accurately forecast future spending. Revenue is relatively stable because contributions are collected automatically and are pre-tax. Income tax revenue fluctuates more with the economy (and is easier to illegally evade).

What guidance does Social Security offer for a better overall tax and budget management system? We need better presentation of Federal government finances. Social Security spending is usually presented in the context of total spending not in relation to its revenues, so we don’t connect the two. Payroll taxes feel like an onerous burden on every pay check. Social Security benefits seem like a burden adding to our public debt. Social Security looks like just one more unfathomably costly activity of an out of control government.

As JohnK commented about an earlier post: “I always grind my teeth when I see social security benefits lumped in as part of our federal budget. For instance, in your “The Purpose and Performance of Our Tax System” post, you have a pie chart showing Social Security benefits as 22% of the federal budget. That amount, and others like it, should be lumped under something like ‘Repayment of Borrowed Money’.” Folks getting Social Security checks are simply getting back contributions they made when they were working, plus the [notional] investment profits.

TonyP commented on another confusing aspect: “I believe it was Al Gore who proposed a “social security lock-box” in order to stop the federal government from looting the social security trust fund to improve cash-flow.” Social Security contributions are not invested as a regular pension fund would in marketable securities, but are used to fund overall Federal spending.

John replied: “As per the Budget Enforcement Act of 1990, the social security trust funds are NOT a part of the federal budget. By law, income accrued by the social security trust funds is invested in securities GUARANTEED as to both PRINCIPAL and INTEREST by the full faith and credit of the U. S. Government. When the government spends the money obtained from these debt obligations or any debt obligations such as Treasury bonds, it is spending “borrowed” money. When it is required to redeem these securities, the amount redeemed should be labeled something to the effect: “Loan Redemptions” and not “Social Security”.

So from one perspective, the Social Security trust fund is a fiction because the money put into it has already been spent, but from another, the money is no more fictional than any other ledger entries representing loans. What was borrowed from the Social Security trust fund is secured by US Treasury bonds that will be repaid. John added: “The official SS history is at: http://www.ssa.gov/history/BudgetTreatment.html Social Security ADMINISTRATION costs are on the federal budget as are administration costs of all federal agencies, but that amount is relatively miniscule, and is not what was represented on Martin’s pie chart.”

Fully absorbing that official history is headache-making but scanning it gives a sense of why presentation is so important. The way our government finances are presented now makes it impossible for most of us to evaluate what’s going on. We don’t know where our tax dollars go. We imagine half is wasted and the other half is spent on things that benefit other people.

In summary:

- We do need a Social Security system

- It is financially sound but if unchanged it will not remain so

- The options to keep it financially sound for at least the medium-term future are not hard to understand

- We are easily misled about all the above because Social Security revenues and spending are usually not presented together, and

- If Social Security finances were presented more clearly we’d be better able to debate what’s most fair to those contributing now, those needing support, and future generations.

But as I’ve said before: “The greatest challenge is … an accelerating reduction in the number of jobs as more and more is done by computers and robots”. That could be a much deeper challenge than for Social Security alone so I will return to it at the end of this series. Next up, Business Tax and Fairness.